- 30 Aug 2022

- Post Views: 6181

-

-

When you apply for a loan, banks and NBFCs evaluate your creditworthiness by analysing your 3-digit credit score as it is one of the most important factors considered by the lenders. A credit score not only determines your eligibility to borrow a loan as an individual but also influences the interest rate.

As a credit score is the backbone of your financial health, it becomes important to improve your credit score and maintain it. However, due to a lack of awareness about the ways to improve it, many of us have poor credit scores. In this blog, let’s understand the ways to improve your credit score:

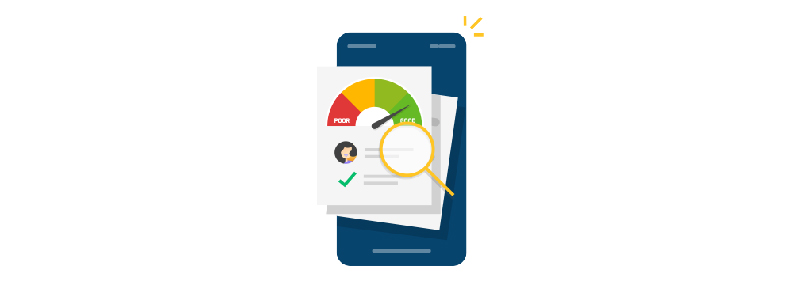

#1 Keep a Regular Check on Your Credit Report: One of the most important things that you must do to improve your credit score is to keep a regular check on your credit report. This way, you will be able to identify errors in your report (if any) that may be pulling down your credit score and will be able to rectify them immediately.

Some common credit report discrepancies are incorrect name/address, closed accounts reported as open, unknown accounts reported in your name, etc. that may be impacting your credit score. Therefore, it is important to check your credit report regularly and keep it error-free as a credit score is calculated on the basis of the information mentioned by various lenders in your credit report.

#2 Maintain a Healthy Credit Utilization Ratio (CUR):

A credit utilization ratio is a ratio of how much credit you are using versus the amount of credit available to you. A CUR is one of the most important factors that is taken into consideration while calculating your CIBIL score.

Ideally, the CUR of an individual should be below 30%. For example, if you have multiple credit cards, it is important to keep a track of how much credit you are using versus your credit limit. If you manage to bring down your credit utilization ratio, you may be able to take your credit score up by a few points.

#3 Start Paying Your Loans/Credit Card Bills on Time:

If you are paying the EMIs of multiple loans and credit card bills, you may be missing on paying the EMIs on time. However, to maintain or build a healthy credit score or to come across as a creditworthy individual to lenders, it is important to plan your finances properly.

Even if you have a lot of EMIs to pay, you are supposed to pay them on time as delayed payments may decrease your credit score. Therefore, set reminders or go for an auto-debit feature to repay all the loans timely.

#4 Have a Healthy Credit Mix: It is always advisable to have a good mix of unsecured loans (credit cards, personal loans, etc.) and secured loans (auto loans, home loans, etc.) of both long and short tenure.

As too many unsecured loans can be viewed negatively by the lenders and may hamper your credit score. However, if you maintain a healthy mix, the lenders may consider you creditworthy.

#5 Limit the Number of Hard Inquiries: There are two types of inquiries that are visible in your credit report – soft and hard inquiries. A soft inquiry occurs when you check your credit report, and it does not harm your credit score. On the other hand, a hard inquiry occurs when you apply for a credit card or a loan and the lender checks your credit report.

Hard inquiries taking place once in a while will not impact your credit score. However, if you apply for multiple loans simultaneously, and a lot of lenders check your credit report within a short span of time, too many hard inquiries will be marked harming your credit score. Therefore, it is advisable not to apply for multiple loans at a time.

#6 Go for Debt Consolidation:

If you have too many loans or credit card EMIs to pay, you can go for debt consolidation and use it to your advantage. You can take a debt consolidation loan from your lender to pay off all your loan/credit card EMIs.

This way, you will only have a single EMI to pay. When you will start paying the single EMI on time and don’t have too many loans being reflected in your credit report, your CIBIL score may gradually improve.

A credit score cannot be built overnight and requires consistent efforts. You must monitor your credit report on a regular basis and pay your debts timely to give a boost to your credit score and creditworthiness.

If you are someone who is facing issues building a credit score or want to understand the factors/myths associated with it, read the DMI Finance Blogs as we bring to you the best information about the finance industry, cyber security, cyber scams/frauds, and a lot more.

Read the DMI Finance Blog and stay connected with us on Facebook, LinkedIn, Twitter, and YouTube for such interesting information.

FAQs

What can boost my credit score?

Paying your EMIs on time and keeping a regular check on your credit report can help in boosting your credit score.

What are the 5 levels of a credit score?

The 5 levels of a credit score are:

Why is my credit score not increasing?

If you are paying all your EMIs on time and your credit score is still not increasing, you must check your credit report either for errors or too many hard inquiries over a short period of time.

What is the lowest credit score possible?

300 is the lowest credit score possible.

What is a good credit score in India?

A credit score of 750 or above is considered to be a good credit score.